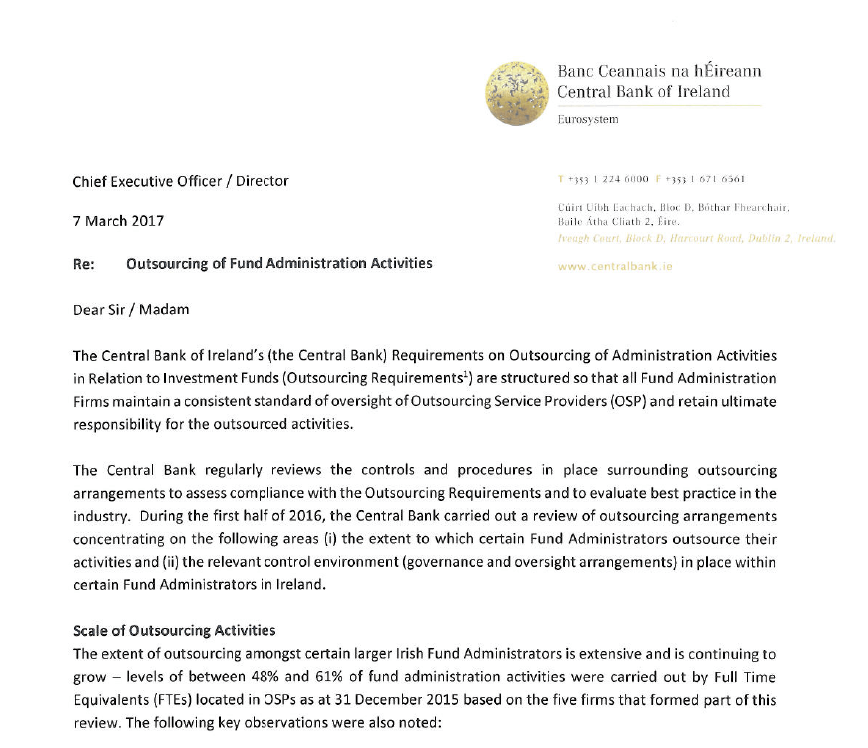

The Central Bank of Ireland this week issued a "Dear CEO" letter outlining concerns over the rising level of outsourcing to global service providers. You can read the letter here.

Based on a thematic review carried out on five of the larger Irish Fund Administrators during the first half of 2016 the Central Bank found that the extent of outsourcing amongst these is extensive and continuing to grow with levels of between 48% and 68% of fund administration activities outsourced as at the end of 2015.

“The Central Bank’s view is that the level of outsourcing observed in this review is likely to be at or close to the outer limit of what is appropriate in the Industry”

That will likely have led to a panicked review of 2017/18 outsourcing plans in several Dublin offices this week.

The Central Bank also made the following observations:

- Firms under review outsourced on average to 10 locations

- Firms under review outsourced primarily to other group entities

- Firms under review were subject to a concentration exposure to one or multiple outsource locations, with these being primarily related to two foreign jurisdictions

From our own observations and what can be deduced from the Central Banks letter, major parts of the valuation of a fund, which is listed as being administered in Ireland is being carried out by another group entity in lower cost countries such as Poland or India. Review and oversight is then carried out in Ireland, allowing it to fall under the regulation of the Central Bank.

How has this trend towards Outsourcing come about?

Over the last 5 years the pace of outsourcing has accelerated. Against a backdrop of increasing costs and lower fees, Fund Administrators are increasingly under pressure to find cost arbitrages for their businesses. As with all businesses there is a constant race to drive revenues and reduce cost, thus growing profits.

The Industry has seen widespread consolidation as firms seek to improve margins through economies of scale. Additionally, several Custodian banks (Goldman Sachs, Credit Suisse, UBS) that have been restructuring their balance sheets post financial crisis have exited Administration. Capital ratios required and relatively low margins have made Fund Admin divisions primary candidates for rationalisation.

Fund Administrators globally have been facing strong headwinds when it comes to increasing revenue. As the Hedge Fund Industry struggles with performance and becomes more populated with Institutional Investors, pressure has been mounting on Fund Managers to reduce fees. The old two and twenty model is officially dead. Managers cost focus has led to knock on fee pressures being put on their service providers, namely Fund Administrators.

With regulation increasing workloads, Fund Admins are caught in a perfect storm of decreasing fees and growing demands from clients. Managers are reluctant to increase fees for handling these additional services. Some Fund Admins are struggling to improve their gross margins above that of a consultancy business model. i.e. more business equals more people and flat to declining profit margins.

In this equation, the only lever you can pull is to reduce the cost of people.

How will this play out long term?

If we play out this trend of outsourcing Fund Administration activities to its long-term conclusion, you’d have to wonder what happens when there are no lower cost centres to move to. Even in perceived lower cost locations we are seeing high inflation and cost savings that could be achieved five years ago, are no longer possible.

The letter issued by the Central Bank also casts doubts over whether regulators will continue to approve the outsourcing of these activities to the level they have thus far.

From a client service perspective Managers are becoming increasingly dissatisfied with the level of outsourcing that is occurring. We’ve heard of cases whereby a Manager used to be able to phone their contact in Ireland to talk through an issue and have it resolved while on the phone. This now requires a ticket being issued that must cycle through several time zones and teams before being fixed. In cases where the Fund Manager is not being passed on the cost saving from this outsourcing, the result is an inferior service for the same price.

Challenges facing Fund Administrators

There is no doubt Fund Administrators face major challenges in the next 5-10 years:

- Increased regulation requiring additional services that clients are unwilling to pay for

- Reduced revenue as fee pressure from Investors continues to trickle down from Managers to service providers

- Increased operating complexity associated with outsourcing across with multiple sites, languages, time zones and cultures

- Fight for talent. More and more companies we speak to are struggling to attract talented graduates as tech companies such as Google, Facebook and LinkedIn appeal more to millennials

Software is eating the world

Some personal observations following on from the Central Banks letter and more generally on Fund Administration trends:

- Few Fund Administrators (if any) have placed technology at the centre of their target operating model

- When 'Software is eating the world' the Fund Administration Industry has bet the house on Outsourcing and continues to rely on people to run its business, albeit in lower cost centres

- The client is no longer the focus. In an ideal world, Fund Administrators take all the pain of running a fund away from Managers so they can focus on making returns and gathering assets. Decisions are being made that are not putting the client’s needs first but instead prioritising cost savings and margins. Fund Managers are not feeling the love

The fallacy of Outsourcing

When you look at the ‘why’ of outsourcing it gives you a few clues as to why this may not be the strategy of tomorrows winning Fund Administrators.

Outsourcing is chosen to reduce costs by moving activities from one location to a lower cost one.

Sounds logical, what could be wrong with that?

A couple of things:

- If an activity is expensive to do in a knowledgeable centre like Ireland, the best thing to do, long term, is automate that process

- By moving it elsewhere, to continue to be carried out by people in a lower cost centre then you get short term marginal gains but further reduce your long-term chances of automation

Reaching the holy grail or facing extinction

As the CEO of a tech company I’m the first to admit that it could appear self-serving to suggest that technology is the solution to the Fund Administrations Industries woes. The Industry already uses technology across its businesses.

For me, what needs to change is how Industry leaders think about technology when it comes to their business in 10 years.

Imagine a world where fund data flows automatically and seamlessly into a single platform that in turn automates the processing, valuation and reporting of a Fund’s NAV. Highly experienced and knowledgeable staff are then freed up to manage the relationship side of the business, delighting Investors and providing Managers with key insights into their business.

That’s the holy grail of Fund Administration.

Few seem to have accepted this reality and should take heed from some famous last words below.

“We didn’t do anything wrong but somehow we lost” Stephen Elop, Former Nokia CEO.

Get our Whitepaper "6 steps to Automating your Reconciliation workflow"

We examine the practical steps when switching from a manual to automated Reconciliation Process.

Our clients include:

Floor 41, 2 Grand Central Tower,

140 East 45th Street,

New York, NY, USA.

Cluster, Floor 2, 16/17 Suffolk Street,

Dublin 2, D02 AT85

Ireland.

ArcLabs Research & Innovation Centre,

WIT West Campus, Carriganore,

Waterford, X91 P20H, Ireland.